TL;DR: In 2026, a 30-day inpatient rehab program typically costs between $5,000 and $30,000 nationally, with a common midpoint of $12,500 to $18,000 and private-facility daily rates of $500 to $650 (national inpatient rehab cost data). In the Dallas-Fort Worth area, actual pricing depends heavily on the program and level of care, but a patient’s real out-of-pocket cost is usually determined more by PPO insurance terms than by the sticker price alone.

A lot of families in Dallas reach the same point before they ever call for help. They know treatment is needed. They may already be searching for a Dallas detox center, looking at inpatient options near Euless, Fort Worth, Arlington, Irving, or North Dallas. Then the financial fear takes over.

That fear is understandable. Many individuals do not purchase inpatient addiction treatment often enough to know its cost, what's included, or what insurance will pay. They see a big number online and assume treatment is out of reach.

The situation is usually more manageable than it first appears. The key is understanding the full financial picture instead of stopping at the advertised program cost.

Table of Contents

- The First Question Everyone Asks About Rehab

- The Average Cost of Inpatient Rehab in 2026

- What Your Investment in Rehab Actually Covers

- Key Factors That Influence Your Final Cost

- How Insurance Makes Inpatient Rehab Affordable in Dallas

- Financing Options and Other Ways to Reduce Costs

- How Tru Dallas Ensures Transparent and Affordable Care

- Frequently Asked Questions About Paying for Rehab

The First Question Everyone Asks About Rehab

When someone finally starts searching for addiction treatment in Dallas, the first question usually isn't about therapy models or amenities. It's cost.

A spouse may be sitting in a parked car outside work, trying to figure out whether inpatient rehab is even possible. A parent in Highland Park may be scrolling late at night after another frightening call. An adult child in Fort Worth may be comparing treatment options for a father who says he wants help but thinks the family can't afford it.

The concern isn't superficial. Cost affects whether a family acts now or delays care. Delay is common when people assume rehab will require a massive upfront payment, or when they don't understand how their PPO plan handles deductibles, coinsurance, and coverage limits.

Many families don't need more motivation to seek help. They need financial clarity so they can say yes to treatment with confidence.

This is where admissions guidance matters. A clear explanation of pricing, insurance, and realistic payment options often lowers the emotional temperature right away. Once the numbers make sense, families can focus on safety, medical needs, and the right level of care.

For anyone asking how much does inpatient rehab cost, the most useful answer isn't a single number. It's a framework.

- Start with the baseline price: Understand the normal range for inpatient care.

- Look at what the program includes: Medical detox, therapy, psychiatric support, and housing all affect value.

- Run insurance correctly: Deductible, coinsurance, and out-of-pocket maximum change the final cost.

- Ask about alternatives: Payment options and lower-cost paths may exist even when coverage isn't ideal.

The Average Cost of Inpatient Rehab in 2026

A family may hear a quote for residential treatment and assume the number is out of reach. In practice, the posted rate is only one part of the decision.

A common national price range for a 30-day inpatient rehab stay runs from about $5,000 to $30,000. Many programs fall somewhere in the middle, while higher-acuity or more private settings can cost more.

That spread is wide for a reason. Inpatient rehab is not a standardized purchase. The final price changes based on length of stay, medical needs, psychiatric support, staffing levels, and whether detox or medication management is part of the admission.

What the national numbers mean

Families often wonder why one facility quotes a far lower rate than another. The difference usually comes from the level of care being delivered, not random pricing.

A daily rate reflects a live-in treatment setting with staff, supervision, clinical programming, meals, and recovery structure built into each day. For someone early in recovery, especially after heavy alcohol, opioid, or polysubstance use, that added support can change both safety and outcomes.

Program pricing often reflects services such as:

- Medical supervision: Monitoring withdrawal symptoms, medication response, sleep disruption, hydration, and physical stability

- Therapeutic programming: Individual counseling, group therapy, recovery education, and relapse-prevention planning

- Mental health care: Evaluation and support for depression, anxiety, trauma symptoms, or other co-occurring conditions

- Housing and daily living support: A protected setting, routine meals, and separation from people, places, and triggers tied to use

This is also why comparing inpatient rehab to weekly outpatient therapy leads families in the wrong direction. Residential care bundles multiple forms of treatment into one controlled setting during the phase when relapse risk is often highest.

Why Dallas area families should look past the headline price

In Dallas-Fort Worth, I encourage families to focus less on the sticker price and more on the likely patient responsibility after insurance. That is the number that determines whether treatment is manageable.

Two people can enter similar residential programs and owe very different amounts. One may still be working through a deductible. Another may have already met much of an out-of-pocket maximum through earlier medical care in the same year. A PPO plan can make the cost far more predictable than families expect once benefits are verified correctly.

For local residents, that matters. A family in Dallas, Plano, Fort Worth, or Euless often needs a fast answer, not a vague range. The useful questions are straightforward: What level of care is clinically appropriate, is the program in network or out of network, and where does the patient stand on deductible, co-insurance, and out-of-pocket maximum?

Practical rule: The posted program rate is the starting point. The number that matters is the estimated out-of-pocket cost after insurance benefits are applied.

That is why admissions and insurance verification need to happen early. A high posted rate does not always mean a high final bill. In many PPO plans, the ceiling is set by the member's remaining out-of-pocket exposure, which gives families a clearer planning target than national averages alone.

| Cost question | Why it matters |

|---|---|

| What is the program rate? | It sets the baseline before insurance applies. |

| What services are included? | It shows whether the price reflects medical and therapeutic care, not just housing. |

| What will the patient owe under their plan? | It determines whether treatment is affordable now, especially under a PPO with a defined out-of-pocket limit. |

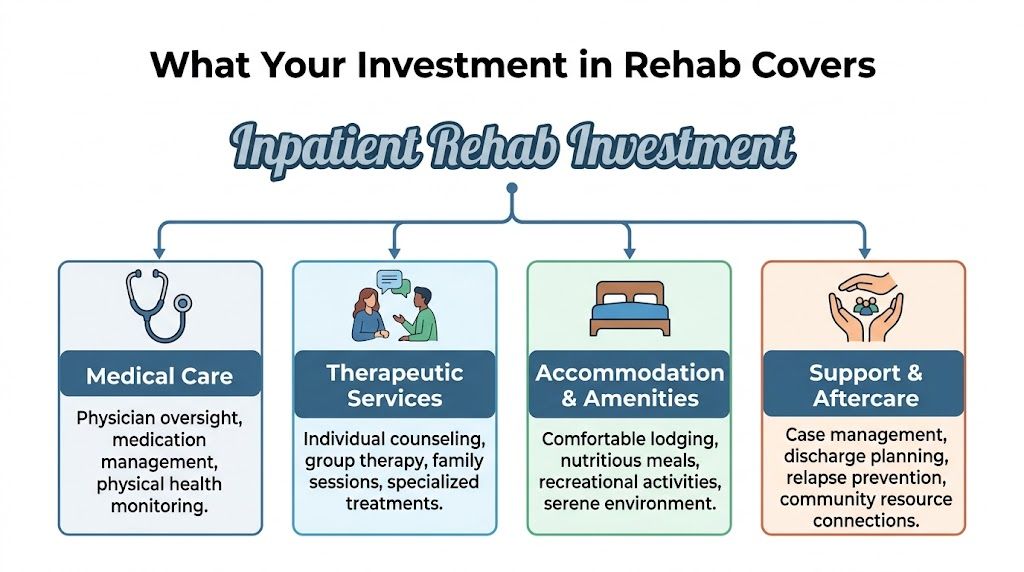

What Your Investment in Rehab Actually Covers

One reason inpatient rehab feels expensive at first glance is that people compare it to ordinary housing or routine counseling. That comparison doesn't work. Inpatient treatment functions more like a fully managed medical and behavioral health stay.

This isn't just room and board

A residential program usually combines several layers of care that would otherwise require multiple providers, multiple appointments, and a much less stable environment.

The first layer is medical support. Early recovery can involve withdrawal symptoms, sleep disruption, appetite changes, blood pressure concerns, cravings, and medication adjustments. Patients don't need to manage that alone.

The second layer is daily therapeutic treatment. Instead of seeing a counselor once a week, patients work through recovery issues in a structured setting with repeated support. That structure matters because the first weeks of sobriety are often when people are most emotionally raw and vulnerable to relapse.

The third layer is the recovery environment itself. Removing access to alcohol or drugs, stepping away from unstable relationships, and spending time in a supervised setting can change the trajectory of treatment.

Common components included in inpatient rehab often involve:

- Assessment and treatment planning: Clinical staff identify substance use history, medical concerns, and mental health needs.

- Detox and stabilization support: Patients who need supervised withdrawal care receive monitoring and symptom management.

- Individual counseling: One-on-one sessions focus on triggers, patterns, trauma, grief, or relapse history.

- Group therapy: Patients build coping skills and learn from others facing similar struggles.

- Family involvement: Loved ones often need education, boundaries, and recovery planning too.

- Medication management: Some patients benefit from psychiatric medications or medication-assisted treatment.

- Meals and accommodations: Recovery is harder when basic physical needs aren't met consistently.

- Discharge planning: Good programs don't stop at discharge. They prepare the next step.

Why integrated care matters financially too

The highest-value treatment isn't always the cheapest on paper. It is often the program that handles the full clinical picture without fragmentation.

A patient with addiction plus panic symptoms, depression, or mood instability often needs more than detox and a few therapy sessions. Without dual diagnosis treatment, the person may leave physically sober but psychologically unprepared. That can lead to a short stay, quick relapse, and another round of crisis care.

The same issue appears with medication-assisted treatment. Someone recovering from opioid or alcohol dependence may need an approach that includes medication, therapy, and close follow-up instead of a one-size-fits-all residential track.

Paying for comprehensive care once is often more practical than paying for repeated emergencies, repeated detox attempts, or treatment that doesn't match the patient's needs.

For Dallas-area families, value is more important than simple price shopping. A lower quote may not be the better financial decision if it leaves out psychiatric care, relapse planning, or continuity after discharge.

A good way to judge value is to ask whether the program addresses these four areas at the same time:

| Care area | What families should confirm |

|---|---|

| Medical | Who monitors withdrawal, medications, and physical safety |

| Psychological | Whether mental health needs are treated alongside addiction |

| Behavioral | How patients build coping skills and relapse-prevention habits |

| Transitional | What happens after discharge and how follow-up is arranged |

Key Factors That Influence Your Final Cost

Two people can ask the same question, how much does inpatient rehab cost, and still end up with very different answers. The final number changes based on treatment length, medical complexity, setting, and whether the program needs to provide specialized services.

Anyone comparing programs should first understand what rehab is, because the term can describe very different levels of care. That difference is one reason pricing varies so much.

Length of stay changes everything

A longer stay usually raises the total cost because the patient is using more housing, staffing, therapy, and clinical resources. But that doesn't automatically make it overpriced.

Some people stabilize quickly and can step down sooner. Others need more time because cravings remain intense, family dynamics are unstable, or co-occurring mental health symptoms haven't settled. For them, extending treatment may be the most practical option.

The shortest appropriate stay isn't always the most affordable in real life. Leaving before the patient is clinically ready can create another interruption, another crisis, and another admission.

Clinical complexity affects pricing

A patient entering treatment for alcohol use with seizure risk has different needs than someone seeking help before withdrawal becomes medically dangerous. A person using opioids daily may need medication support and closer observation. A person with depression, trauma, or bipolar symptoms may need psychiatric care built into treatment.

These are not luxury add-ons. They are often core parts of safe care.

Key drivers often include:

- Detox intensity: Some substances create a more medically demanding withdrawal process.

- Dual diagnosis care: Mental health conditions can require added psychiatric attention.

- Medication-assisted treatment: MAT may improve stability for patients with opioid or alcohol dependence.

- Relapse history: People with repeated treatment attempts often need a more individualized plan.

A program should fit the patient's clinical reality, not the family’s preferred budget number. Choosing too little care often costs more later.

Amenities and setting still matter

Not every price difference is clinical. Some of it comes down to privacy, room type, campus style, and comfort level. A patient may prefer a quieter setting, more personal space, or a higher-end environment. Those factors can raise cost even when the core treatment model is similar.

That doesn't mean comfort is irrelevant. For some patients, privacy and a calm environment improve participation and reduce the urge to leave early. But it's still important to separate clinically necessary services from optional amenities.

A simple way to compare programs is to ask these questions in order:

- What level of medical and psychiatric care is included

- How much treatment is individual versus group based

- What support exists after discharge

- Which parts of the price reflect comfort rather than treatment

A Dallas family comparing options near downtown, North Dallas, Las Colinas, or the Mid-Cities should keep the focus on fit. The best financial decision is usually the one that balances safety, therapeutic depth, and realistic affordability.

How Insurance Makes Inpatient Rehab Affordable in Dallas

For many families, insurance is the difference between feeling shut out of treatment and realizing rehab is within reach. PPO plans can be especially useful because they often provide some flexibility in where the patient receives care. But flexibility only helps when the plan is interpreted correctly.

The most common mistake is stopping at the coinsurance number. Families hear that the plan covers a certain portion of treatment and assume they can estimate the bill from that alone. That's often incomplete.

The four insurance terms that matter most

A few terms control the out-of-pocket math.

- Deductible: The amount the patient may need to pay before insurance starts sharing more of the cost.

- Coinsurance: The share the patient pays after the deductible, based on the plan's terms.

- Copay: A fixed payment attached to some services, depending on the policy.

- Out-of-pocket maximum: The annual ceiling on what the patient has to pay for covered care under the plan.

Of those four, the out-of-pocket maximum is the one families miss most often. It can change the financial picture dramatically.

The hidden cost ceiling most families miss

Many patients don't realize that the out-of-pocket maximum creates a built-in cap. One example shows why this matters. A $10,000 program with a $1,000 deductible and 80% coverage appears to leave the patient paying $2,800. But if the plan has a $2,500 out-of-pocket maximum, the patient's total responsibility is capped at $2,500 instead (out-of-pocket maximum example for rehab insurance).

That single detail can make treatment feel far more possible.

For Dallas-Fort Worth residents with PPO insurance, this is the question worth asking before anything else: What is the remaining out-of-pocket maximum for this year, and how would inpatient rehab apply toward it?

A quick coverage review often answers issues such as:

- Has the deductible already been met

- Is the facility considered in-network

- Does prior authorization apply

- How much remains before the out-of-pocket maximum is reached

- Which services count toward that limit

Here is a simple illustration of how PPO math can shift the actual cost.

Sample Out-of-Pocket Costs with PPO Insurance

| Total Rehab Cost | Insurance Plan Details | Patient's Total Out-of-Pocket Cost |

|---|---|---|

| $10,000 | $1,000 deductible, 80% coverage, $2,500 out-of-pocket maximum | $2,500 |

| $20,000 | PPO plan with in-network benefits and an out-of-pocket maximum that caps covered patient responsibility | Often lower than a basic deductible-plus-coinsurance estimate |

| Residential stay over multiple covered services | Deductible, coinsurance, and covered charges accumulate toward the annual maximum | Can stop increasing once the plan ceiling is met |

That is why a real insurance verification matters more than generic estimates. A person may assume they owe far more than they do.

A fuller explanation of this process appears in does insurance cover inpatient rehab, especially for families sorting through policy language under time pressure.

Why in-network and out-of-network costs can look so different

Network status changes pricing because insurers and facilities usually operate under different reimbursement terms depending on the contract. In practical terms, in-network care often gives patients more predictable costs, clearer benefit rules, and a better shot at having more of the bill treated as covered care.

Out-of-network care can still be worth exploring with a PPO. But families should ask harder questions:

- What percentage of out-of-network care is covered

- Will the insurer apply a different deductible

- Will part of the bill fall outside the insurer's allowed amount

- Can a written estimate be provided before admission

- If coverage is denied, what appeal options exist under parity protections

Federal law requires mental health and addiction treatment to be covered comparably to other medical services, but that doesn't mean approval happens automatically. It means patients and families should push for a clear explanation when costs or denials don't make sense.

Insurance doesn't make rehab free in every case. It does make the cost more predictable when someone reviews the deductible, network status, and out-of-pocket maximum together instead of separately.

For families in Dallas, Plano, Grapevine, Arlington, or Fort Worth, that review is often the turning point. Once the true ceiling is clear, treatment decisions become much less intimidating.

Financing Options and Other Ways to Reduce Costs

Insurance isn't the only lever. Some patients have limited benefits, high deductibles, or a preferred program that creates a gap between covered services and total cost. That doesn't mean treatment is out of reach.

Ways families usually close the gap

Some solutions are straightforward. Others require a few calls and a little persistence.

- Payment plans: Some facilities let families spread out deductible or coinsurance costs instead of paying everything at once.

- Healthcare financing: Medical loans can help when treatment is urgent and the family needs time to repay.

- HSA or FSA funds: Many families forget to check whether pre-tax healthcare dollars can be used for covered treatment expenses.

- Family contribution planning: Sometimes several relatives can each cover a manageable part rather than one person carrying the whole burden.

- In-network selection: If more than one clinically appropriate option exists, choosing an in-network setting may reduce the immediate financial load.

People also benefit from general strategies to reduce healthcare costs when they're organizing a larger treatment budget. The principle is simple. Use every available benefit before assuming the full charge must be paid out of pocket.

Questions worth asking before ruling treatment out

A lot of patients leave money on the table because they don't know what to ask. Admissions and billing teams can only answer the questions they hear.

These are the questions that often uncover the best path:

- Can the deductible be divided into scheduled payments

- Does the facility offer any reduced-rate arrangements in certain cases

- Can HSA or FSA funds be applied to the patient portion

- Is there a lower-cost but clinically appropriate level of care after stabilization

- Are there local or state-supported options if private treatment isn't workable

Families looking for alternatives can also review free rehab in Dallas and low-cost addiction treatment options when private insurance coverage isn't enough.

Cost should be treated as a planning problem, not as an automatic reason to delay care.

What doesn't work is assuming the first number is final, or comparing programs only by monthly price without asking what's included. What usually works is combining benefits review, realistic budgeting, and a clear clinical recommendation.

How Tru Dallas Ensures Transparent and Affordable Care

Financial stress often drops when a facility gives the family a plain-language estimate before admission instead of vague assurances. That should be the standard.

What financial clarity should look like

A good admissions process doesn't just ask for an insurance card. It reviews the patient's benefits, explains likely patient responsibility, identifies whether the plan is in-network or out-of-network, and flags issues that could affect approval or timing.

For Dallas-area patients who need residential support after detox, inpatient treatment at Tru Dallas Detox & Recovery Center is one option that includes insurance verification as part of the admissions process. That kind of review helps families understand cost before they commit, rather than after a bill arrives.

The most helpful financial conversations usually answer these points clearly:

- What level of care is being recommended

- Which insurance benefits appear to apply

- What the likely patient portion may include

- Whether any payment arrangements are available

- What next steps are needed for admission

Patients and families dealing with addiction treatment in Dallas rarely need more complexity. They need direct answers, respectful communication, and a realistic path forward.

When cost is the main barrier, the next best step is usually a confidential insurance verification call. That conversation can turn a vague fear into a concrete plan.

Frequently Asked Questions About Paying for Rehab

Will rehab show up on a credit report

Treatment itself doesn't function like a public record. The larger concern is whether unpaid medical debt is eventually sent to collections. Families should ask about billing terms upfront so there aren't surprises later.

Can a deductible be paid over time

Sometimes, yes. It depends on the facility's financial policies. Many families should ask directly whether the patient portion can be divided into manageable payments rather than paid all at once.

Is luxury rehab worth paying more for

Sometimes the extra cost reflects comfort, privacy, or setting rather than stronger clinical care. A higher-priced program may be worthwhile if it improves engagement or meets a specific personal need, but families should separate essential treatment services from optional amenities before deciding.

Can HSA or FSA funds be used

In many cases, they may be usable for qualified healthcare expenses connected to treatment. The safest move is to confirm the eligible charges with the plan administrator and the treatment provider before admission.

What should a family ask on the first call

The most useful questions are practical ones. Ask what level of care is recommended, what insurance appears to cover, what the estimated out-of-pocket responsibility may be, and what happens if the first authorization period needs to be extended.

What if treatment still feels unaffordable

The worst move is silence. When families call and explain the obstacle clearly, they often learn about payment arrangements, lower-cost pathways, or public and low-cost resources they hadn't considered.

If cost is the main thing holding a family back, Tru Dallas Detox & Recovery Center can help clarify the numbers. A confidential call can review insurance, explain likely out-of-pocket responsibility, and help a patient or loved one understand the next step toward safe treatment in the Dallas-Fort Worth area.